Explore Australia's booming energy storage market—federal policies, state incentives, tech trends, and real-world case studies. See future growth forecasts.

1. Introduction

In recent years, as the global transition to a low-carbon economy accelerates, Australia's energy storage market has seen unprecedented growth opportunities. The federal and state governments have actively promoted renewable energy and energy storage technologies through policies, incentives, and subsidy schemes. Particularly in the next five years (2025–2030), as energy system transformation gains momentum, battery and inverter technologies will continue to advance, showcasing their strengths in residential, commercial and industrial (C&I), and generation-side applications. This article explores Australia's energy storage market prospects by analyzing policy dynamics, market projections, technological pathways, and case studies. It also highlights future market trends and tech advancements through comparisons of product specs, market shares, and cost structures.

2. Policy Framework Analysis

2.1 Federal-Level Policies

The Australian federal government has fostered a favorable policy environment for energy storage through strategic initiatives, including:

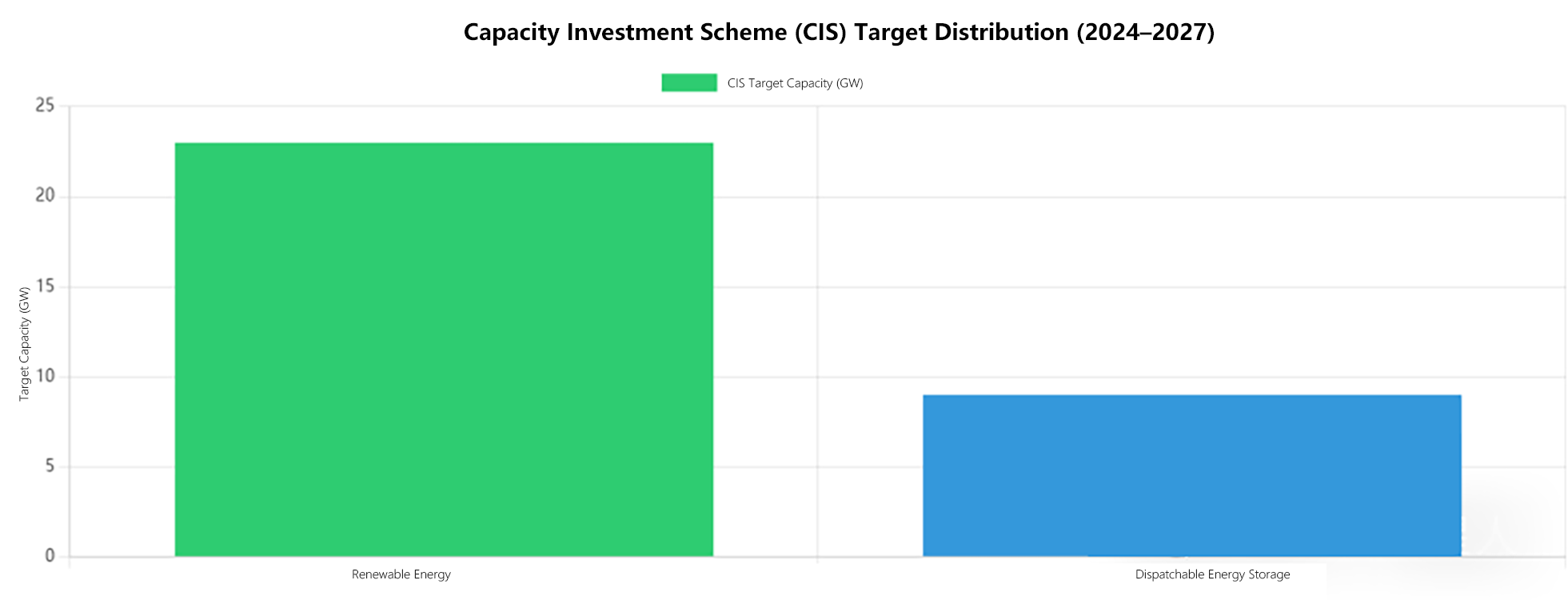

(1) Capacity Investment Scheme (CIS)

Launched between 2024 and 2027, the CIS targets 32 GW of new clean energy capacity (23 GW renewables + 9 GW dispatchable storage). Via semi-annual tenders (National Electricity Market, NEM) and annual tenders (Wholesale Electricity Market, WEM), it offers long-term revenue guarantees and tax incentives to mitigate investment risks.

(2) Renewable Energy Manufacturing and Industry Support Plan

Under the "Future Made in Australia" strategy, the government will invest AUD 22.7 billion over a decade to boost domestic clean energy manufacturing. This includes the Solar and Battery Breakthrough Initiative, critical minerals tax relief, and local battery supply chain development—strengthening Australia's foothold in the global energy market while supporting storage innovation and deployment.

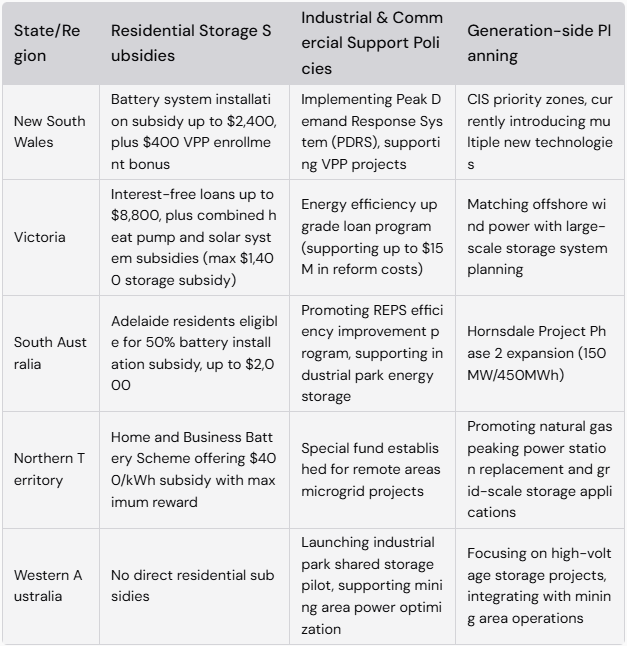

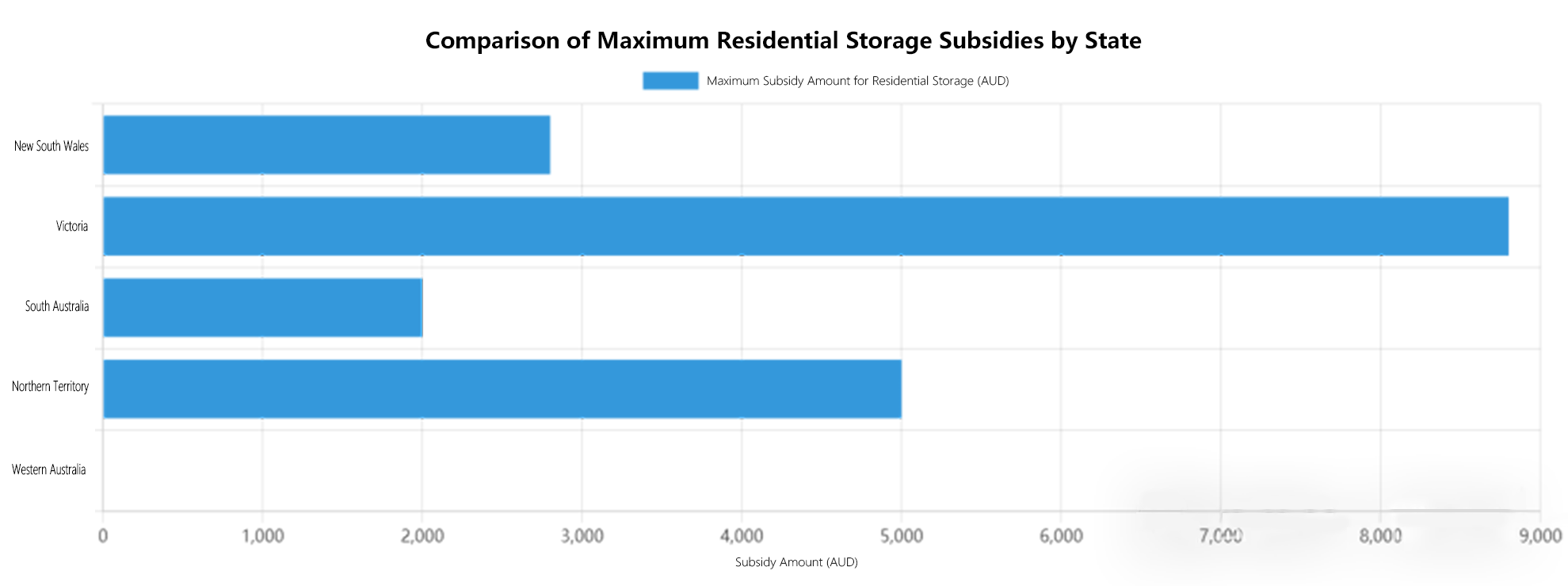

2.2 State-Level Comparisons

Federal policies set the direction, while states refine implementation through targeted incentives.

These policy measures address the requirements of energy storage projects across various scales, application scenarios, and regional variations. They vary not just in subsidy levels, while also focusing on supporting the integration of storage systems into markets, participation in grid ancillary services, and supply chain infrastructure development.

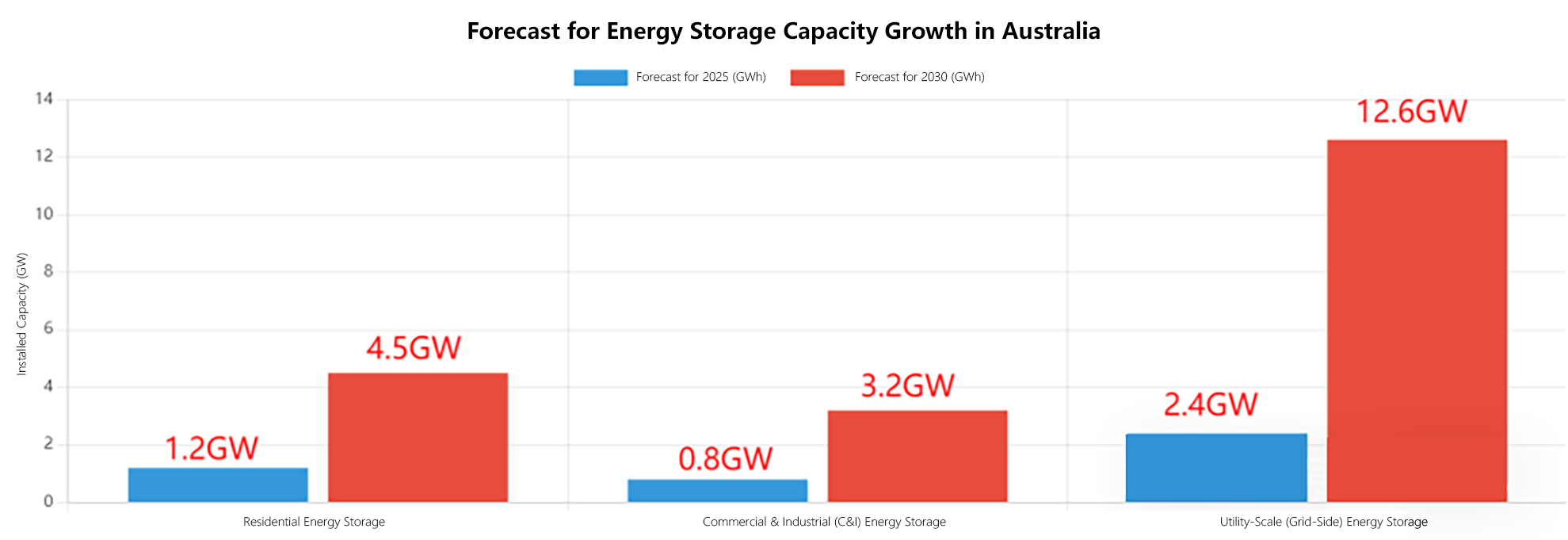

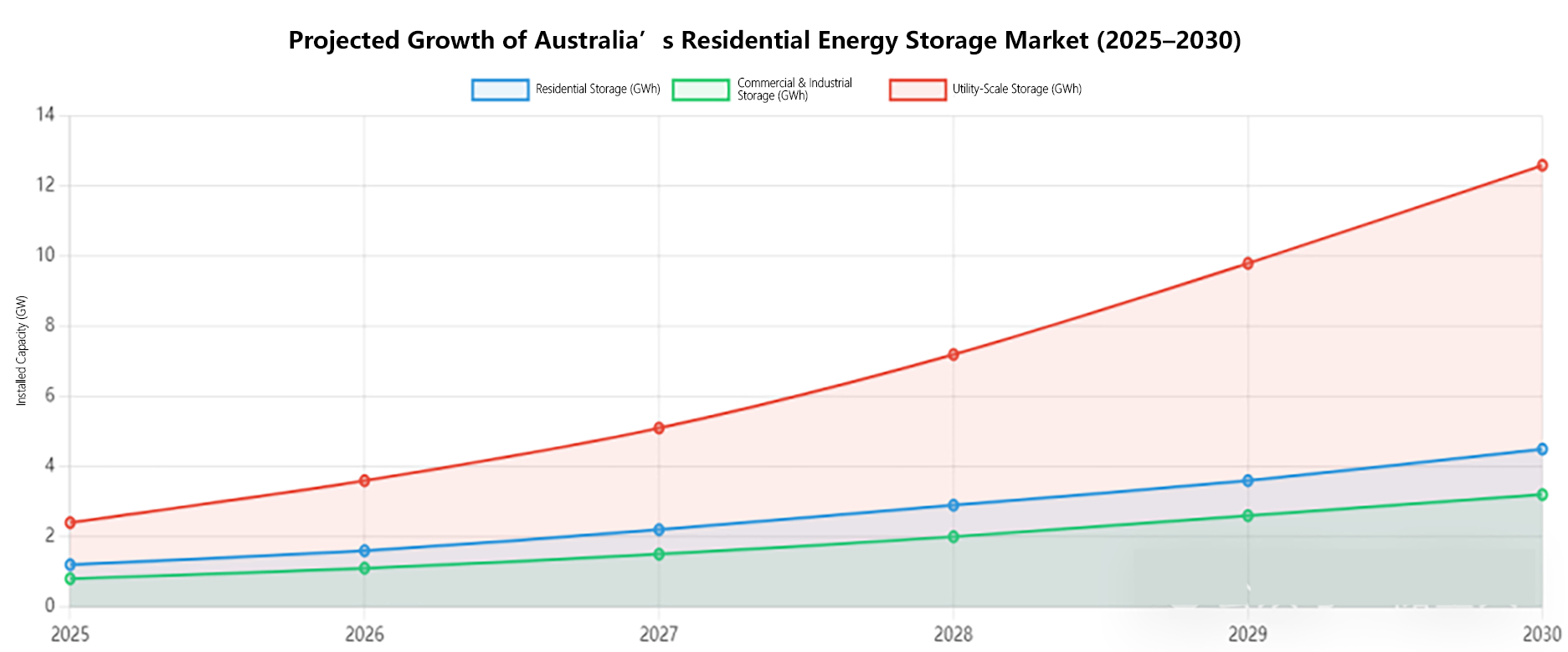

3. Market Size

3.1 Capacity and Growth Forecasts.

According to the latest market research reports and BNEF data, global newly installed energy storage capacity in 2024 has reached a historic high. Supported by policies such as the Clean Energy Innovation Strategy (CIS), energy storage applications in Australia are expected to continue growing rapidly over the next five years.

With the declining costs of distributed photovoltaic systems and maturing supporting storage systems, home energy storage systems will become increasingly popular. On the other hand, utility-scale commercial, industrial, and power generation projects will be deployed at scale through competitive bidding processes and long-term contracts.

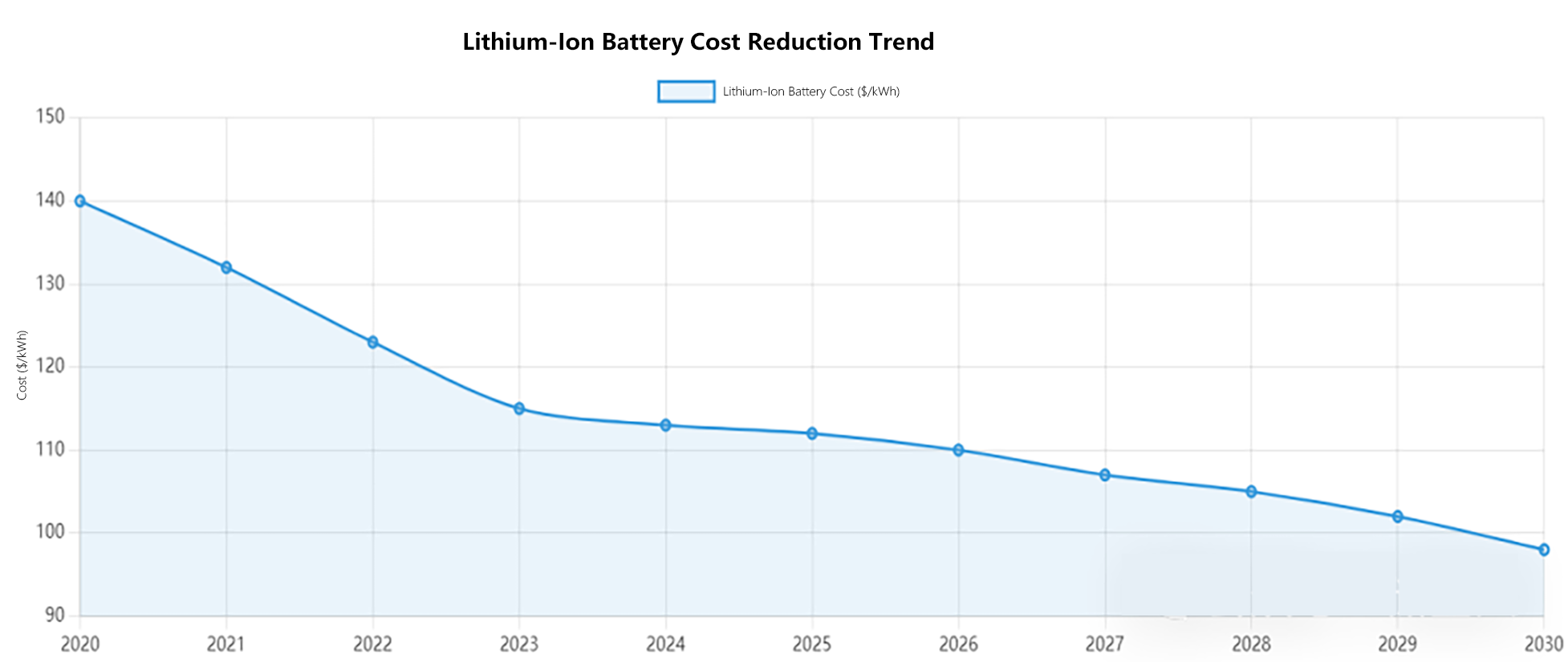

3.2 Cost Reduction Trends.

Economies of scale, improved local production, and advanced techniques have slashed lithium battery costs—from $115/kWh (2023) to a projected $112/kWh (2025), with a sub-$100/kWh target by 2030.

Major Tech Drivers:

- LFP market share rising to 65%

- Solid-state batteries nearing commercialization

- Local production cutting costs

Lithium iron phosphate (LFP) batteries, prized for safety and lifespan, dominate adoption. Emerging tech like solid-state and flow batteries also progress. Better cost-efficiency will further spur demand.

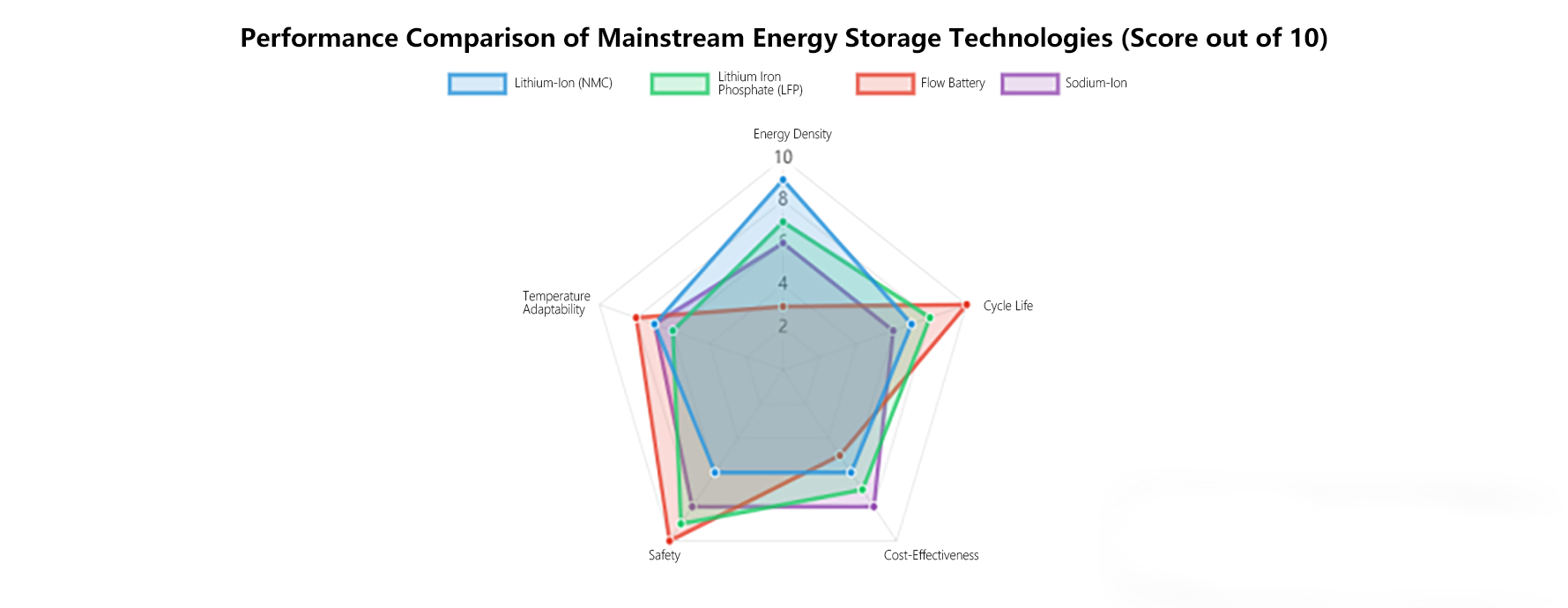

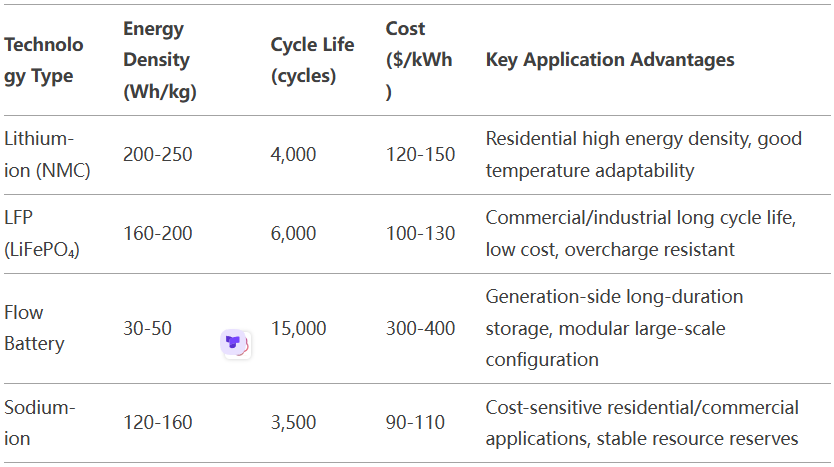

4. Technology and Product Comparisons

4.1 Key Storage Technologies Parameters And Applications.

The Australian market currently has several main energy storage technologies, each with unique technical specs and key benefits for different uses.

Since different battery technologies vary in material composition, installation methods, and management systems, projects should be designed based on usage needs and cost efficiency. For home energy storage systems, high energy density and compact size matter more, while for commercial, industrial, and utility-scale projects, system longevity and operational efficiency are more important.

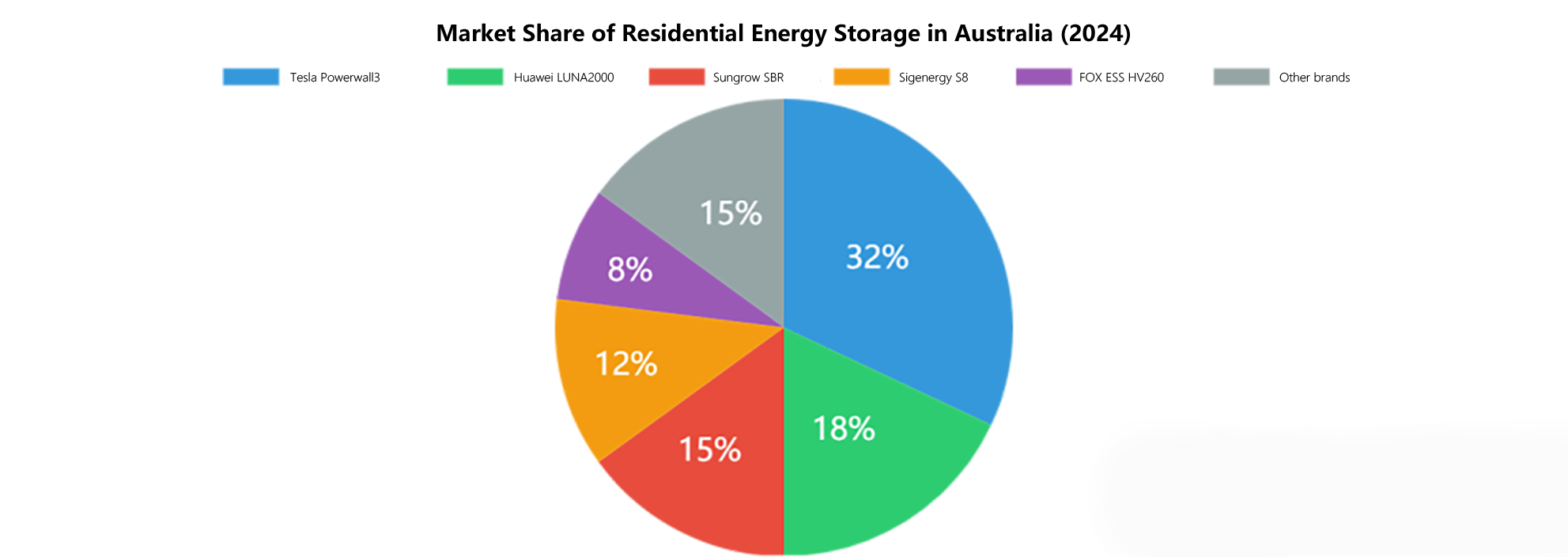

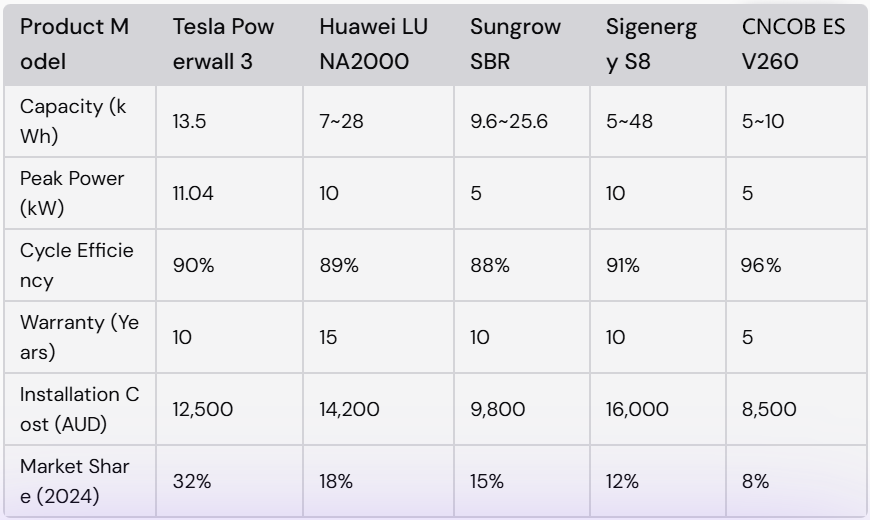

4.2 Residential Energy Storage Products Comparison

In Australia's residential energy storage market, several major brands are locked in fierce competition. The following table lists the top five leading residential energy storage systems currently available, comparing metrics such as capacity, peak power, round-trip efficiency (energy retained during charge/discharge cycles), warranty period, installation cost, and market share:

The table shows that Tesla's Powerwall 3 maintains a significant market share thanks to its outstanding energy density and strong brand recognition. Huawei's LUNA2000 excels in battery life and warranty coverage, making it ideal for energy-intensive homes. Other brands like Sungrow, Sigenergy, and CNCOB respectively have their own strengths in installation costs and scalability, so customers can choose based on their specific needs.

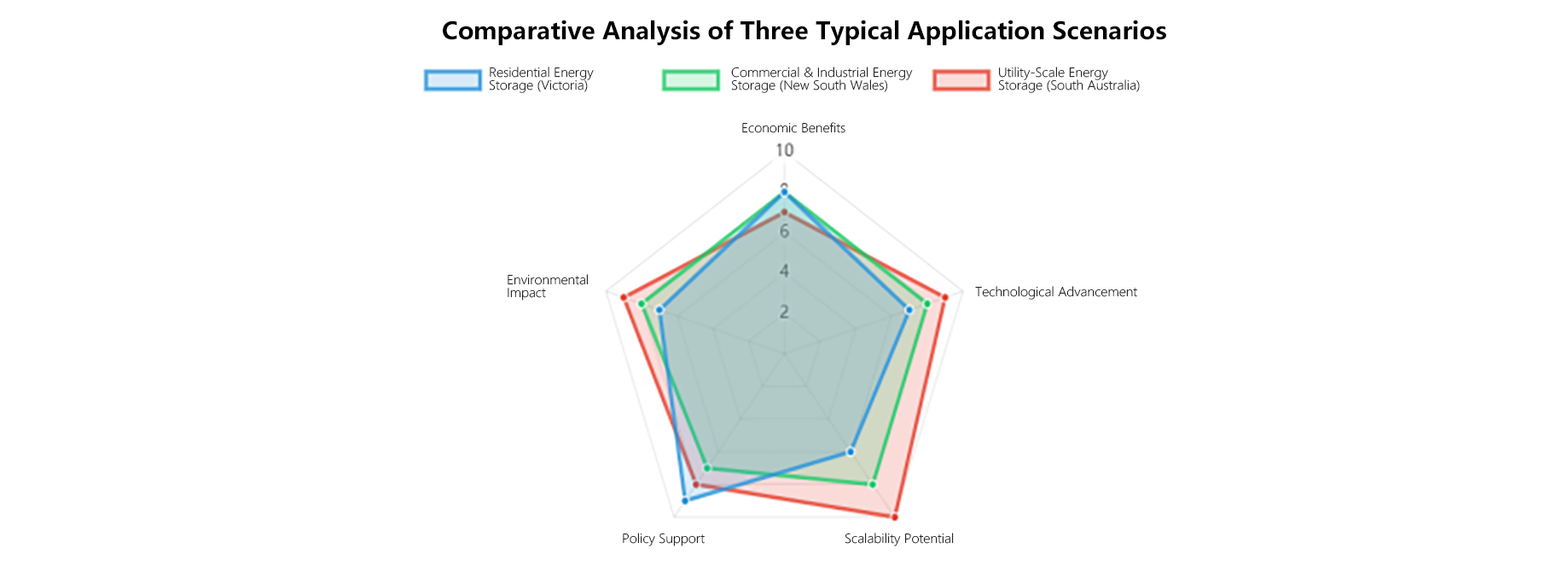

5. Case Studies of Application Scenarios

Energy storage projects in Australia are gradually transitioning from pilot phases to large-scale commercialization. Different battery technologies and system configurations demonstrate unique advantages across various application scenarios, as illustrated in the following three representative cases:

5.1 Residential Energy Storage Case – Victoria Model

Case Description

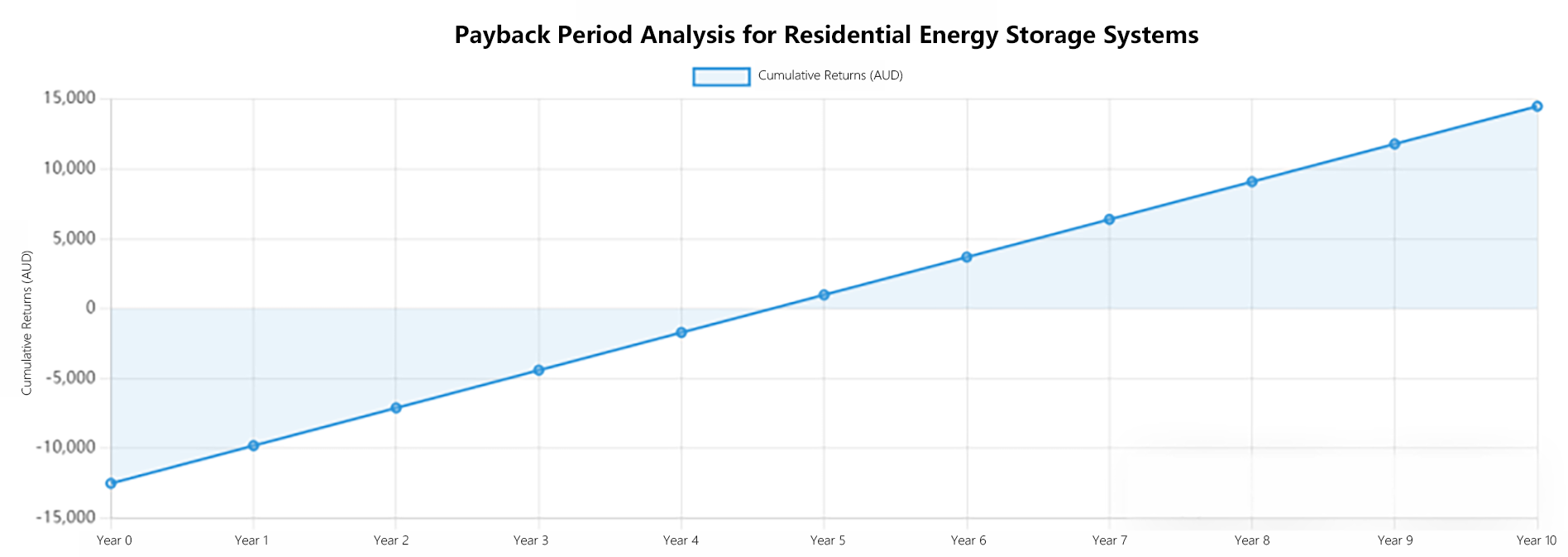

In the suburbs of Melbourne, Victoria, a standard household adopted a 10kW solar PV system paired with a 13.5kWh Tesla Powerwall 3 energy storage system. The project leveraged state government-provided interest-free loans (up to AUD $8,800) and solar rebates (up to AUD $1,400), significantly reducing the household’s initial investment.

System & Economic Benefits

- System Configuration: 10kW solar PV + 13.5kWh storage module

- Policy Utilization: Interest-free loans and additional subsidies lowered installation costs

- Economic Benefits:

- Electricity bills were cut to 22% of their original amount, saving approximately AUD $2,300 annually

- Participation in a Virtual Power Plant (VPP) generated additional income of around AUD $400/year

- Estimated payback period: approximately 6.2 years

This case highlights the synergy between state-level subsidies and federal strategies, enhancing both the economic viability and environmental benefits of residential energy storage.

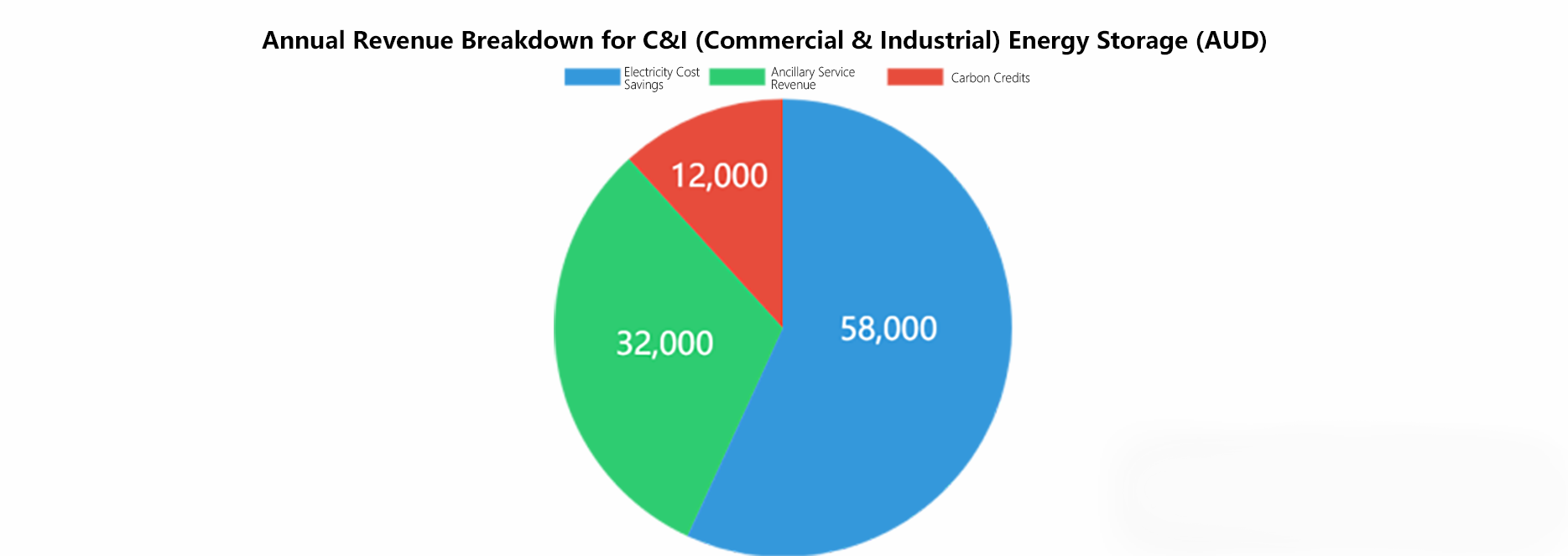

5.2 Commercial & Industrial Storage Case – New South Wales Virtual Power Plant (VPP) Integration

Case Description

A large logistics center in Sydney deployed a 500kW/2MWh Huawei LUNA2000 storage system, primarily for smoothing solar PV fluctuations, participating in grid ancillary services, and implementing peak shaving and valley filling. With state-led battery subsidies and VPP incentives, the project improved energy utilization while delivering substantial revenue.

Key Benefits

- Electricity Savings: Approximately AUD $58,000 annually

- Ancillary Service Revenue: Around AUD $32,000/year

- Revenue from Carbon Credits: Approximately AUD $12,000/year

This project not only reduced energy costs through technology optimization but also achieved multi-channel revenue via the VPP platform, serving as a benchmark for commercial storage applications.

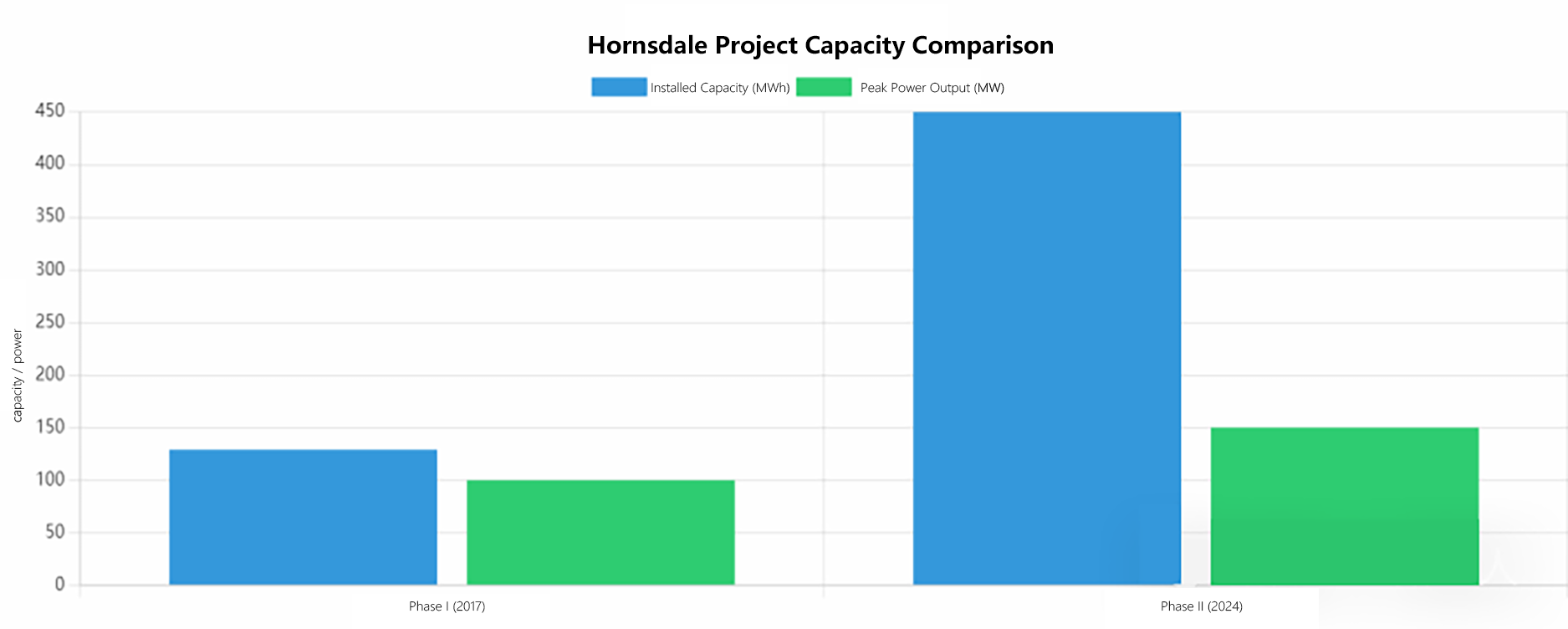

5.3 Grid-Scale Storage Case – South Australia’s Hornsdale Project

Case Description

The Hornsdale Energy Reserve in South Australia is a globally renowned grid-scale storage project. Since 2017, Phase 1 (100MW/129MWh, pure lithium-ion) has significantly improved regional grid stability. The 2024 Phase 2 expansion adopted a hybrid lithium-ion/flow battery system, scaling capacity to 150MW/450MWh.

Technical & Economic Benefits

- Technology Upgrade: Hybrid storage improved long-duration storage economics and operational efficiency.

- Core Advantages:

- Grid inertia response time under 100ms

- Black-start capability (ability to restart without external power) covering 15% of regional load

- Levelized Cost of Energy Storage (LCOES) dropped to approximately AUD $0.11/kWh

- Policy Incentives: Federal and state support reduced funding pressure, accelerating expansion.

This case exemplifies the shift toward high-capacity, large-scale, and long-duration storage, showcasing its critical role in grid stability and renewable integration.

6. Challenges & Future Recommendations

6.1 Key Bottlenecks

Despite Australia’s promising storage market, challenges persist:

- Grid Connection Delays: Average approval timelines of 22 months hinder project progress.

- Inadequate Standards: Performance and safety criteria for long-duration storage require refinement.

- Supply Chain Risks: High import dependency (e.g., 73% for lithium batteries) demands localized production.

- Market Volatility: Rapid tech advancements (e.g., emerging solid-state batteries) disrupt existing markets.

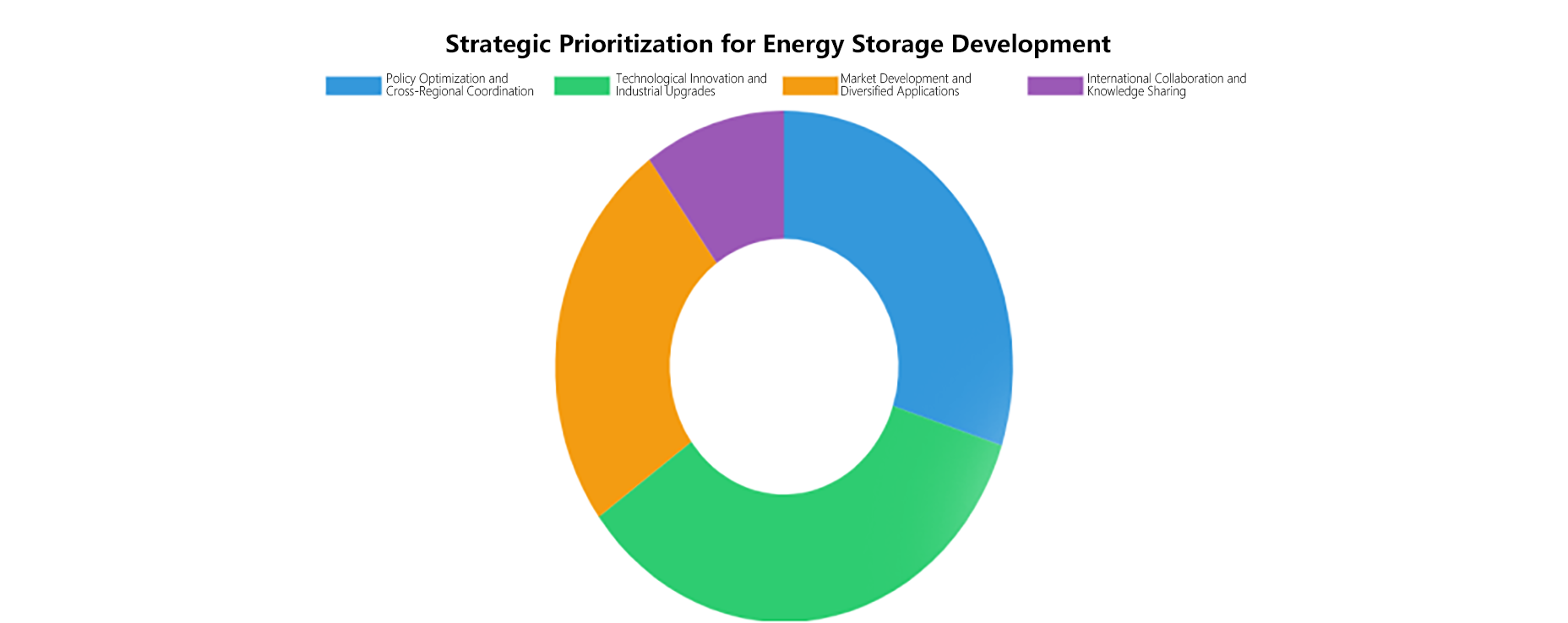

6.2 Strategic Recommendations

1.Policy Optimization & Cross-Sector Collaboration

Streamline grid approvals, establish inter-state storage trading, and unify market data platforms.

Refine long-duration storage standards with targeted incentives.

2.Technology & Industry Advancement

Boost R&D for emerging solid-state and flow batteries via a AUD $200 million fund.

Support local supply chains through tax breaks and low-interest loans.

3.Market Diversification

Promote energy storage asset-backed securities (ABS) to attract long-term investors.

Enhance VPP platforms and flexible energy-use mechanisms for tailored residential/commercial solutions.

4.Global Collaboration

Adopt best practices from the U.S. and Europe in grid integration and system design.

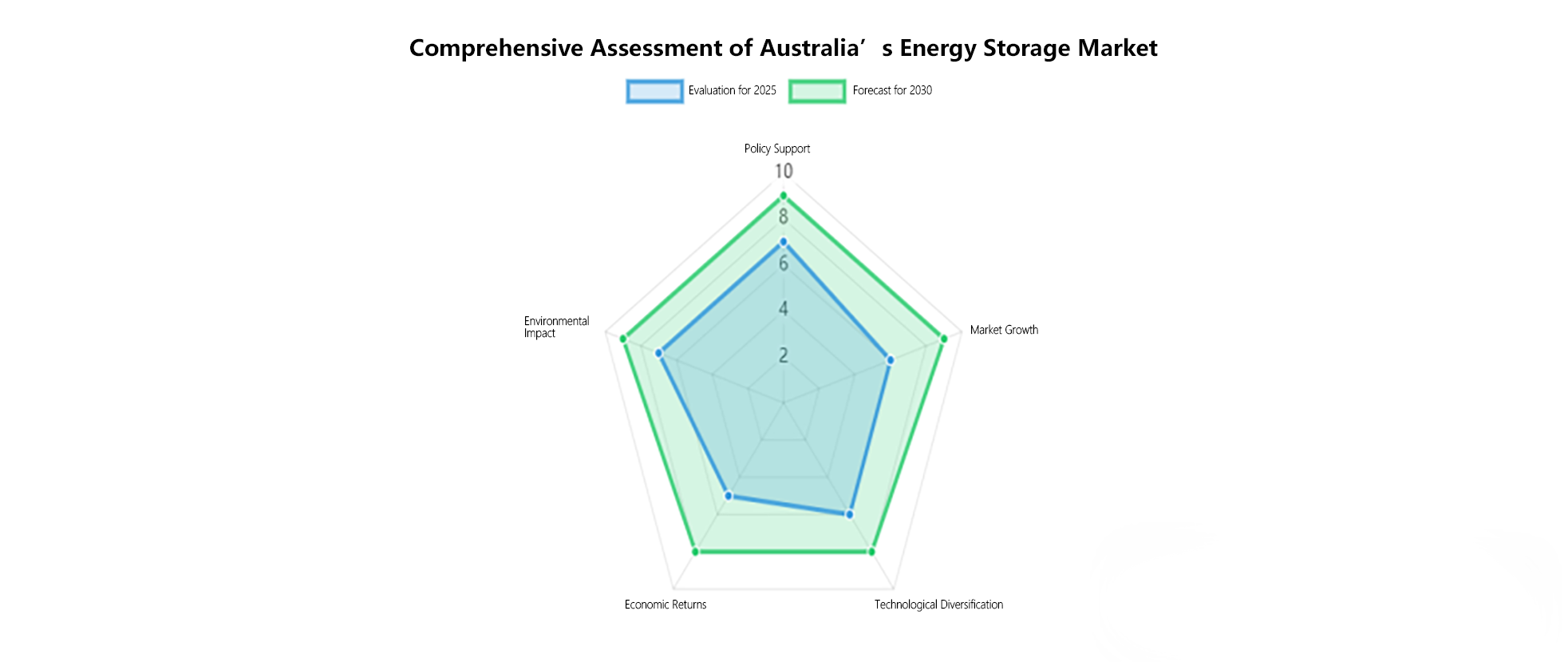

7. Conclusion

Australia’s energy storage market holds vast potential across policy, technology, market, and application scenarios over the next five years.

Policy-Driven Advantages

- Federal Capacity Investment Scheme (CIS) and manufacturing grants provide robust support.

- State-level differentiated policies foster diverse regional markets.

Market Expansion

- Compound annual growth rate (CAGR) of 30–40% across sectors (2025–2030), led by grid-scale storage.

- Falling storage costs will further stimulate demand.

Diverse Technologies

- NMC/LFP dominate, but flow, sodium-ion, and emerging solid-state batteries are commercializing.

Demonstrated Success Cases

- Residential, commercial, and grid-scale projects validate economic and environmental benefits.

- New South Wales’ VPP and South Australia’s Hornsdale project offer valuable implementation models.

Challenges & Strategies

- Grid delays, standards gaps, and import reliance require policy refinement, R&D, and continuous innovation.

Through these measures—optimized incentives, lower funding barriers, and international collaboration—Australia is poised to become a global model for storage deployment within five years.